After a week of extreme turmoil in the Middle East, due to the killing of Iranian IRGC leader Soleimani, Iran’s 2nd in command, and the Iranian missile retaliation, global media and analysts are getting convinced that there is room for negotiation.

U.S. President Trump stated that he is open for dialogue with Iran, a move that calmed markets worldwide. Oil prices, which had spiked on the risk of an all-out war between the US and Iran and the possible fall-out for oil and gas production in the region, are now falling back to pre-Soleimani assassination levels.

OPEC Secretary-General Mohammed Barkindo and UAE’s Energy Minister Suhail Al Mazrouei added to this bearish sentiment by saying that there is no risk of an oil shortage if hostilities do flare up. Al Mazrouei also reiterated that he doesn’t see any risk that Iran will close the Strait of Hormuz. This was confirmed by his Iranian colleague Zanganeh, who claimed that the crisis is profitable for Iran as oil and gas prices increased. These official statements need, however, to be taken with a truckload of salt. OPEC’s confidence that there is enough spare capacity in the market, and that there is ample supply, is a political statement to quell existing fears. The spare capacity of OPEC is at present almost totally in the hands of two main players, Saudi Arabia and the UAE, while the rest of the members are struggling to reach even their own set targets. In case of a military confrontation between Iran (or proxies) and the US, a real possibility exists that total OPEC spare capacity is taken out. No other producer could substitute a possible loss of Saudi oil production.

In reality, the crisis in Iran and Iraq will have a much larger impact than experts at Top-5 banks and trading houses are currently anticipating. At the same time, media reporting is biased, looking for possible light at the end of the tunnel, while taking any positive statement made by Washington, Riyadh-Abu Dhabi or Tehran as fact. The conflict is not over, you could even say that the current status of the conflict is like a smoldering peat-fire. You can feel the heat but you don’t see the flames.

Assessments of last week’s developments have been largely looking at conventional military reactions. The Iranian missile attack on US forces in Iraq has been without casualties, reported in the media as a low-intensity retaliatory strike by Iran. The reality is more diffuse. Tehran has understood at present that an all-out military reaction, leading to a lot of US or Western casualties, was not going to be beneficial to the cause of the Mullahs. However, a reaction to Soleimani’s killing was demanded by extremist forces inside of Iran and its proxies. To expect that this will be the only reaction by Iran is naive. Trump has upped the ante, and Iranian leader Khamenei and his IRGC compatriots will almost certainly react in kind. Several scenarios need to be addressed by analysts and be integrated in their oil and gas assessments. Forget the Strait of Hormuz as the risks for Iran are likely higher than for its direct opponents. Other options are more likely.

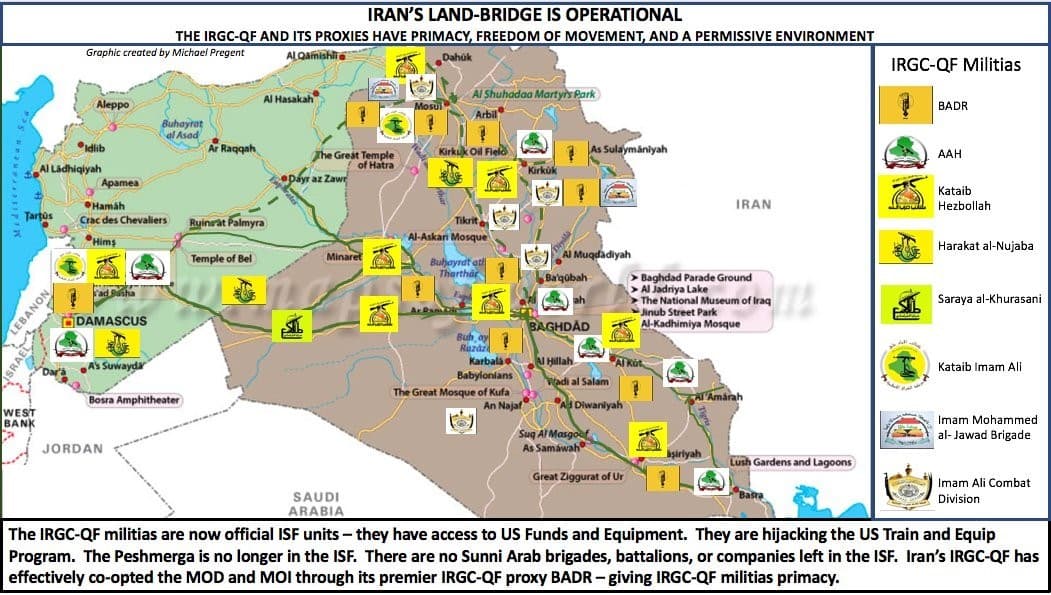

A proxy response via Hezbollah, Hamas or the pro-Iranian Shi’a militias in Iraq, against the main oil and gas operations of Western and Arab national oil companies now seems the most likely reaction. This type of response can be executed by proxies at a low cost, as these targets are easily accessible and high profile. Even without the direct involvement of Iran (IRGC), Tehran can put immense pressure on its Arab neighbors while at the same time hitting Western and Asian economies. Next to this, Tehran could escalate the proxy war by Hezbollah or Hamas against Israel.

Even if no direct war is expected, as indicated by UAE Energy Minister Suhail today at the UAE Energy Forum in Abu Dhabi, experts expect that energy and water sectors in the Arab countries could be targeted. As shown by the Abqaiq attack, all these operations are very vulnerable to drones or possibly cyberattacks. By striking critical infrastructure, Iran and proxies will be able to destabilize not only the economies of the GCC region, but deal a blow to global economies too.

A real asymmetric war threat is the use of cyberattacks to bring down specific or nationwide assets, such as oil-gas assets, desalination and power plants (IWPP). Tehran already has threatened to start a cyberwar against the U.S. and its allies, but at present no actions have been reported. Saudi Aramco, ADNOC or BAPCO could be targeted. Qatar’s energy installations are less vulnerable, looking at the reasonably strong relations between Doha and Tehran. Qatar, however, could get caught in the crossfire because of its large U.S. and Western military presence.

More worrying could be a cyberattack or even missile attack on energy-water projects, as this type of infrastructure is crucial for the entire region. A proxy or asymmetric war strategy by Iran is the most feasible and will be hard to counter by the West or Arab states. The Mullah regime understands its options. A full-scale attack on Saudi Arabia or Abu Dhabi, or a military confrontation in Iraq will be met this time by a large military reaction by U.S. President Trump, with possible support of his NATO partners.

Looking at the current situation, Iranian leader Khamenei and his cohorts will need to react soon. A long delay will be considered a sign of weakness. WWIII can be virtually ruled out as Iran is too weak and the Western-Arab alliance has not yet got enough men on the ground. Proxy wars will continue to plague the region, and these conflicts could escalate further if Iran continues its current nuclear program.

The above scenarios could all have a detrimental impact on oil and gas production and exports from the world’s most important hydrocarbon region. Taking out Saudi or UAE oil infrastructure will remove spare capacity with a bang. Just the disruption of Iraqi oil supply could cause a shock in the world’s oil markets. Geopolitics are real and even if the risk premium in oil prices seems to be fading, analysts should not ignore the current risks in the Middle East, The East-Mediterranean and Libya.

By Verocy for Oilprice.com